All Categories

Featured

:max_bytes(150000):strip_icc()/indexed-universal-life-insurance.asp-Final-9f72d52f11d643c693ab8b3600f3cd27.png)

[/image][=video]

[/video]

Withdrawals from the cash worth of an IUL are typically tax-free up to the quantity of premiums paid. Any type of withdrawals above this amount may be subject to taxes depending on plan structure.

Withdrawals from a Roth 401(k) are tax-free if the account has been open for at the very least 5 years and the individual is over 59. Possessions withdrawn from a traditional or Roth 401(k) prior to age 59 may sustain a 10% penalty. Not exactly The claims that IULs can be your very own financial institution are an oversimplification and can be misinforming for lots of reasons.

You may be subject to upgrading linked health and wellness concerns that can influence your ongoing prices. With a 401(k), the cash is constantly yours, consisting of vested employer matching despite whether you give up adding. Danger and Guarantees: Most importantly, IUL plans, and the cash worth, are not FDIC insured like common savings account.

While there is commonly a flooring to protect against losses, the growth possibility is covered (indicating you may not fully benefit from market growths). The majority of professionals will certainly agree that these are not similar products. If you want death benefits for your survivor and are worried your retired life savings will not suffice, then you may intend to think about an IUL or various other life insurance policy item.

Certain, the IUL can provide access to a cash money account, but once again this is not the main function of the product. Whether you desire or require an IUL is a highly private inquiry and relies on your primary monetary purpose and objectives. Nonetheless, listed below we will attempt to cover benefits and limitations for an IUL and a 401(k), so you can additionally delineate these items and make a much more informed decision pertaining to the finest method to handle retired life and caring for your loved ones after fatality.

Wrl Freedom Global Iul Review

Financing Expenses: Finances against the plan accumulate interest and, otherwise settled, decrease the survivor benefit that is paid to the beneficiary. Market Participation Restrictions: For many plans, investment development is linked to a securities market index, but gains are typically covered, restricting upside prospective - indexed universal life insurance companies. Sales Practices: These policies are commonly marketed by insurance coverage representatives who may stress benefits without totally clarifying expenses and risks

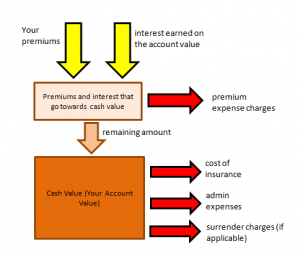

While some social networks pundits recommend an IUL is an alternative product for a 401(k), it is not. These are different products with various purposes, functions, and costs. Indexed Universal Life (IUL) is a sort of irreversible life insurance policy policy that likewise provides a cash money value element. The money value can be utilized for several functions including retired life financial savings, additional revenue, and various other financial requirements.

{kind=link}

Latest Posts

Universal Index Life Insurance Pros And Cons

Iul Quote

Universal Life Insurance Quotes